The VC-LP Relationship: How VCs Keep Investors Coming Back And Investing In Successive Funds

Learn how VCs build lasting LP trust through transparency, communication, and discipline—driving loyalty and faster fundraising.

Venture capital is, at its core, a relationship business. The VC-LP relationship - aka, the partnership between a general partner (GP) and a limited partner (LP) – decides whether capital returns for the next fund or drifts elsewhere. When the LP relationship status is healthy, capital calls close promptly, co-investment invitations flow, and quarterly updates turn into collaborative strategy sessions. When trust erodes, fundraising slows, and legal costs spiral.

So, what is a LP relationship in practical terms? It is a long-term alliance built on clear communication, disciplined portfolio construction, and full transparency around fees, valuations, and governance. Put simply, what is the VC LP relationship if not an ongoing exchange of insight and shared upside?

This guide explains how to build that partnership, from setting early expectations through consistent reporting to reinforcing alignment over multiple fund cycles—so your next raise relies on loyalty rather than luck.

The Evolution of VC-LP Engagement Models

Early-stage venture began as an insiders’ club—small partnerships, handshake agreements and one-page summary letters. As institutional money replaced family offices in the 1990s, expectations around reporting, governance, and strategic dialogue grew.

- 2000s: Institutional Limited Partners Association (ILPA) formed and published its first reporting guidelines, giving LPs a baseline for net-asset-value (NAV) statements.

- 2010s: Quarterly webinars and annual meetings became standard, but information remained one-way.

- 2020s: Data portals, continuation funds and co-investment sidecars shifted the conversation from “here is our data” to “here is how you can act on it.” ILPA’s 2025 Reporting Template 2.0 now mandates look-through fee disclosures and ESG metrics, raising the bar for transparency.

LPs today expect real-time dashboards, on-demand capital-account statements, and proactive guidance on liquidity solutions such as NAV loans or secondary sales. Funds that deliver see higher loyalty scores and faster closings. Bain & Company calls this “professionalizing fundraising”—the act of matching institutional service standards with venture-style agility.

Operationalizing LP Trust: Best Practices for GPs

Build Familiarity Through Consistent, Multi-Channel Communication

ILPA recommends quarterly financials plus a “flash” update within 15 days of major exits. Top-quartile managers go further: brief emails after term-sheet signings, short Loom videos before capital calls, and investor days that rotate across geographies. NVCA’s 2025 Yearbook highlights that funds with at least three touchpoints per quarter recorded 15 percent higher re-up rates in 2024.

Operate With Re-Up Diligence in Mind

LPs rarely drop a relationship because of one bad vintage; they disengage when patterns of under-delivery emerge. Keep a “re-up file” that tracks every KPI investors will scrutinize: DPI trajectory, loss ratio, reserve usage and key-person stability. Share that file ahead of fundraising so there are no surprises.

Institutionalize Transparency and Reporting Standards

Adopt ILPA’s template wholesale. Populate it with portfolio-company-level data, fee allocations and ESG metrics. Automate the process so reports arrive on the same day each quarter. GPs that implemented version 2.0 of ILPA’s template cut ad-hoc investor data requests by 35 percent on average. Rolling these reports into a secure investor portal with instant alerts deepens engagement and signals operational excellence.

Articulate Investment Rationale and Portfolio Construction Decisions

During frothy markets, some managers chased every hot sector. In the current slower era, deviation from a defined investment style undermines credibility.. McKinsey & Companylists “strategy discipline” as one of five alphas that separate outperformers from the pack. Tie every deal back to the original thesis and show how allocation limits keep the fund diversified. Providing look-through exposure charts alongside cash-flow forecasts demonstrates disciplined capital deployment and helps LPs benchmark performance expectations.

Equip LPs to Advocate Internally

Many institutional investors must justify allocations to an investment committee. Provide slide decks, case studies, and benchmarking comps they can lift directly into their IC memos. Bain’s latest Private Equity Outlook stresses that GPs who “arm LPs with talking points” close funds six months faster on average.

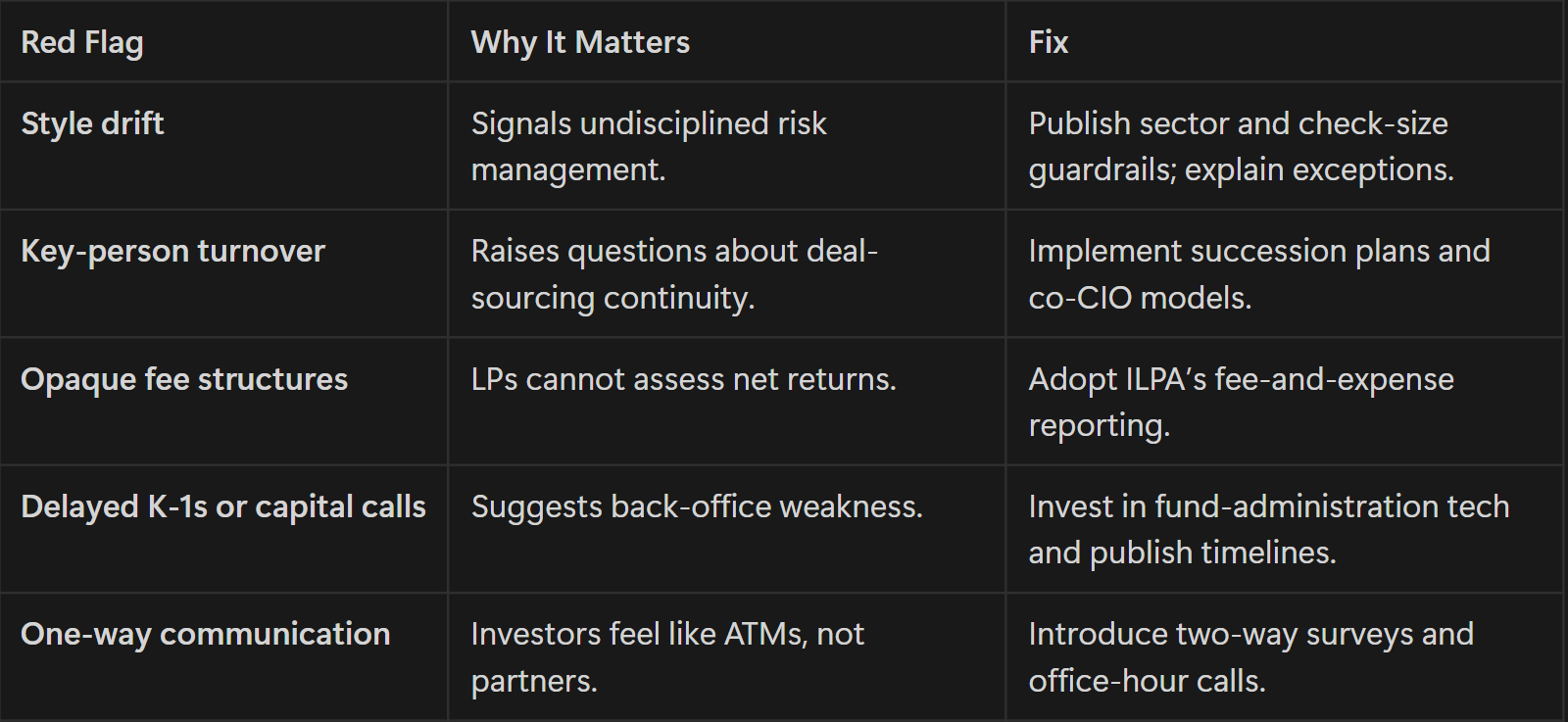

Red Flags That Undermine LP Confidence

CAIA’s due-diligence framework flags these issues as early warning signs that LPs should discount a manager.

Industry bodies such as the Chartered Alternative Investment Analyst Association (CAIA) and the Institutional Limited Partners Association (ILPA) give LPs a clear playbook for spotting trouble. CAIA’s “Red Flags in Private-Markets Due Diligence” series warns that cues like style drift, unexpected key-person turnover, and chronically late reporting often precede both underperformance and operational failures, while ILPA’s updated Due Diligence Questionnaire pushes allocators to probe fee transparency, valuation controls, and emerging ESG metrics.

Once any of these signals surface, investors widen reference checks, ask for supplemental data, and may earmark future commitments elsewhere. The most trusted GPs therefore benchmark themselves against these frameworks in advance, hence closing gaps, documenting improvements, and communicating fixes before LPs even have to ask.

Relationship-Driven Fundraising: LP Loyalty as a Strategic Asset

Venture fund economics suggest that capital “stickiness” is fast becoming the biggest driver of a GP’s cost of capital—and, by extension, its competitive edge. Fresh figures in the 2025 NVCA Yearbook show that nearly 80 percent of all dollars committed to U.S. venture vehicles in 2024 came from LPs already backing the same managers. highlighting a decisive flight to familiarity. The picture tightens at the firm level: just 30 franchise managers captured 68 percent of commitments of $500 million or more, according to the PitchBook–NVCA Q4 2024 Venture Monitor.

Why does that matter? Because re-ups are dramatically cheaper and faster to close. Bain & Company’s 2025 Global Private Equity Report notes that once a GP has an established LP roster, legal fees and placement-agent costs drop to roughly one-third of what it takes to land first-time investors, while time-to-first-close can compress by six to nine months—freeing partners to focus on sourcing and portfolio support instead of endless roadshows.

Performance follows loyalty. Analysis of more than 2,500 U.S. venture funds by Cambridge Associates shows that vehicles with long-tenured LP syndicates generated pooled net IRRs 400 basis points above public-market equivalents over the past decade, partly because predictable capital lets GPs time exits for value, not optics.

The virtuous cycle extends to fundraising resilience. The McKinsey Global Private Markets Review 2023 found that LPs who feel known by their managers are far more willing to over-allocate in choppy markets, reinforcing a loop of loyalty and liquidity that strengthens a fund’s ability to seize opportunities when others are capital-constrained.

Taken together, the evidence is clear: cultivating LP loyalty is no longer an investor-relations “nice-to-have.” It is an operating discipline equal in importance to deal sourcing and portfolio value creation. GPs that measure satisfaction, map churn risk, and assign clear relationship owners are already pulling ahead on fundraising velocity, fee economics, and, ultimately, net returns.

Conclusion

Long-run venture performance hinges on more than finding the next unicorn. It depends on cultivating an LP relationship status that feels collaborative, data-driven, and transparent. GPs who communicate consistently, anchor every decision in the original mandate, and equip investors with decision-ready information see higher re-ups, lower fundraising costs, and more strategic flexibility.

For firms ready to modernize their investor-relations stack, Fundingstack centralizes LP contacts, streamlines the process of drafting and sending updates, and tracks engagement metrics—turning relationship management into a repeatable process instead of a heroic effort.

FAQs

What defines a long-term LP-GP relationship?

A multi-fund commitment where capital, co-investment, and knowledge sharing flow in both directions. ILPA characterizes it by repeat commitments, proactive communication, and alignment on strategy and fees.

What are early indicators of LP disengagement?

Declining attendance at annual meetings, slower responses to capital calls, and rising ad hoc data requests often precede a decision not to re-up. CAIA lists these as priority red flags in due diligence checklists.

How frequently should GPs engage with LPs?

Quarterly financials are the minimum. High-performing funds add monthly portfolio snippets and real-time alerts on material events, a cadence linked to 15 percent higher re-up rates in NVCA’s 2025 Yearbook.

How can emerging managers build institutional-grade trust?

Start with ILPA-style reporting from day one, invite LPs to ride along on diligence calls and secure an independent fund administrator to validate valuations. Bain’s Private Equity Outlook finds that first-time funds adopting these practices raise 30 percent more capital on average.